Nigeria’s fintech revolution has fundamentally transformed how millions save their money, with Opay emerging as a formidable challenger to traditional banking giants like GTBank, UBA, and Access Bank. As Nigerians increasingly seek higher returns on their savings amid economic challenges, the interest rate divide between digital platforms and conventional banks has sparked intense debates across social media platforms from Lagos to Abuja.

The numbers tell a compelling story that’s reshaping Nigeria’s financial landscape. While traditional banks offer average savings rates of just 5.32% according to Central Bank of Nigeria data, Opay’s savings products deliver up to 18% annual interest – more than triple what most conventional banks provide. This dramatic disparity has triggered a massive migration of Nigerian savers from traditional banking halls to mobile apps, creating one of Africa’s most significant financial disruptions.

The Social Media Verdict: Why Nigerians Are Choosing Fintech

Across Twitter, Instagram, and TikTok, the sentiment is overwhelmingly clear – Nigerian users are abandoning traditional banks in droves. “Peace of mind wan finish Opay users,” commented one social media user, capturing the prevailing mood among fintech adopters. This phrase has become a rallying cry for millions who’ve experienced the frustration of bank downtimes while Opay users continue their transactions seamlessly.

Recent polling by Technext revealed Opay as Nigeria’s most preferred banking app in 2024. The survey highlighted key advantages driving this preference: zero transfer fees, instant transactions, and crucially, those higher interest rates that traditional banks simply cannot match. “OPay’s built-in support is good but slow. However, banks are worse,” noted one comprehensive app review, reflecting the comparative satisfaction levels.

YouTube reviews consistently praise Opay’s user experience, with popular tech reviewer MissTechy noting that “transfers to Opay accounts averaged around three to four seconds while transfers to other bank accounts averaged around five seconds”. This speed advantage, combined with superior interest rates, creates a compelling value proposition that traditional banks struggle to counter.

However, the social media narrative isn’t entirely one-sided. Some users on platforms like Nairaland and Trustpilot have raised concerns about customer service delays and transaction disputes. “Good at first until my 8,000 naira vanished without trace,” complained one Trustpilot reviewer, highlighting the challenges that can arise with digital-first platforms.

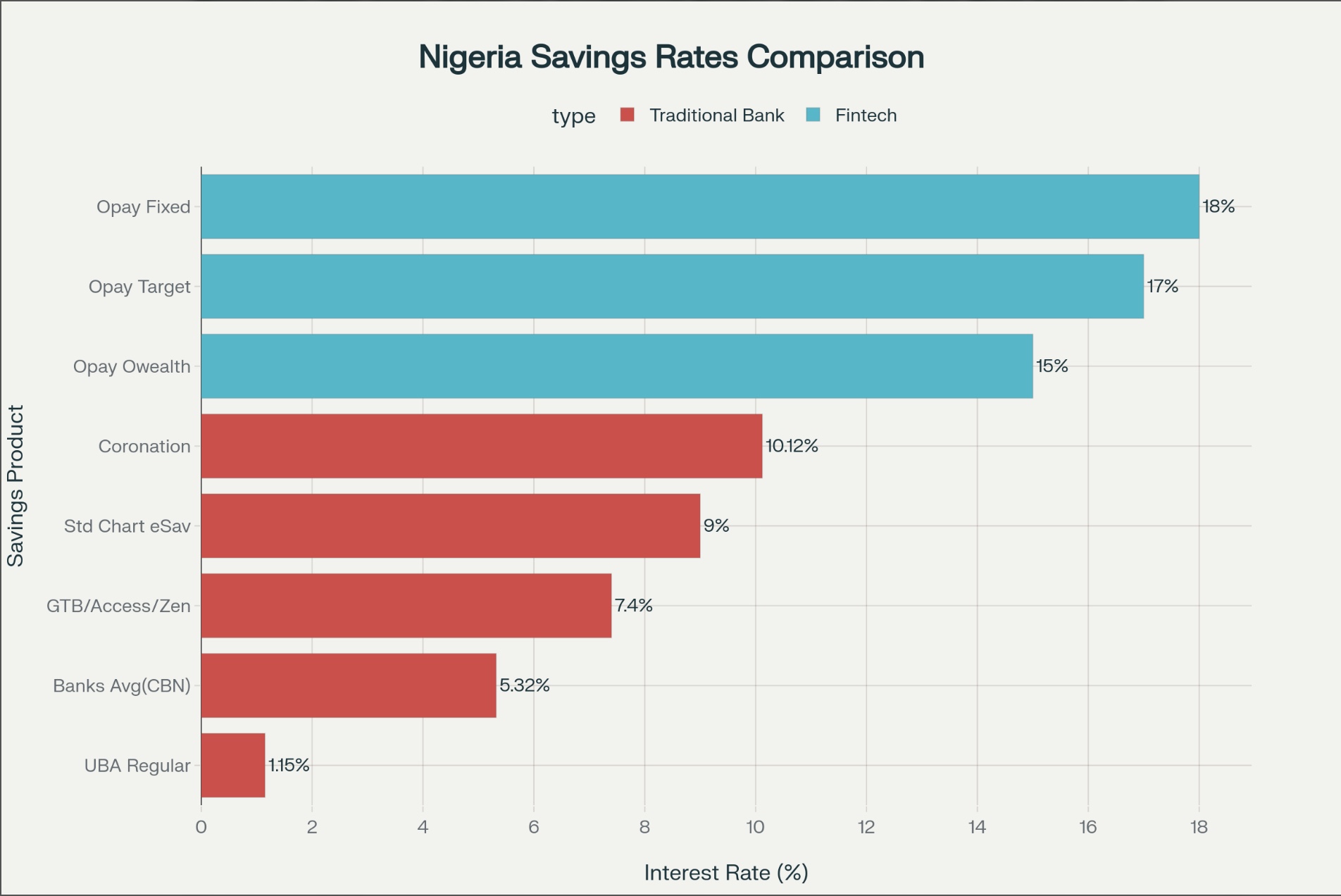

The Numbers Game: How Interest Rates Stack Up

The mathematical reality is stark and undeniable. Opay’s Owealth flexible savings offers 15% annual interest with daily liquidity – meaning you can withdraw anytime while earning returns that dwarf traditional banking options. Their fixed savings products push this even higher, reaching 18% for longer-term commitments, while Target Savings delivers 17% for goal-oriented savers.

Traditional banks present a markedly different picture. UBA’s regular savings account offers a mere 1.15% annually, while the broader banking sector averages 5.32% according to CBN data. Even premium products like Standard Chartered’s eSaver, offering up to 9% interest, fall significantly short of fintech alternatives.

This disparity reflects fundamental differences in operational costs and business models. Traditional banks maintain expensive branch networks, larger staff complements, and legacy IT systems that drain profitability. Fintech platforms like Opay operate with minimal physical infrastructure, passing these cost savings to customers through higher interest rates and reduced fees.

The competitive pressure has forced some traditional banks to raise their rates. BusinessDay reported that 18 deposit money banks now offer 7.4% interest following CBN’s monetary policy adjustments. However, this reactive increase still trails fintech offerings by substantial margins, suggesting structural limitations in traditional banking’s ability to compete on pure interest rate terms.

Coronation Bank stands as a notable exception among traditional institutions, offering 10.12% interest – the highest among conventional banks. Yet even this premium rate falls short of Opay’s basic Owealth product, illustrating the magnitude of the fintech advantage.

Banking experts explain this gap through operational efficiency metrics. “Digital banks often offer lower fees and higher interest rates on savings accounts because they don’t have the overhead costs associated with physical branches,” notes financial analysis platform DECTA. This structural advantage appears sustainable, suggesting the interest rate gap may persist long-term